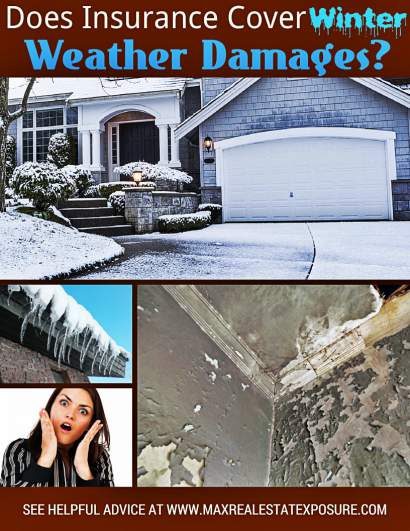

Are you wondering about winter insurance and if your home is protected?

Winter weather can be rough on homes and their inhabitants. Winter is known for its hazards, from sub-zero temperatures to wet ice sheets.

But you have even more to worry about if you are a homeowner. Winter can cause severe damage to your home, leading to expensive repairs.

The question is, will your homeowner’s insurance cover the cost of damages?

This is on the minds of many when we go through brutal winters. Thinking about blizzards, high winds, slippery roads, emergency vehicles, and downed power lines doesn’t make me look forward to winter.

The good news is winter insurance will cover most damage from storms.

Making sure you do not let too much time pass between when the damage occurred and filing a claim is essential!

If you are walking around your home and have just discovered winter damage you were not aware of, get on the phone right now and contact your insurance carrier.

From many years owning multiple homes in different states and being in the real estate industry, winter insurance is a necessary expense that shouldn’t be taken lightly.

If you live in a cold-weather climate it is imperative to have a winter insurance policy that will cover your property in the event of damages.

Let’s examine everything you should know about winter insurance. You will love the tips if falling tree branches and downed power lines plague your area!

Noteworthy Facts

1. Winter insurance covers damages and accidents during the winter season.

2. It typically includes coverage for home damage caused by harsh winter weather conditions like snowstorms and ice dams.

3. It can protect against burst pipes and water damage, common issues during freezing temperatures.

4. Studies show that 8 out of 10 claims made during winter are related to snow and ice damage.

5. Over 60% of homeowners with winter insurance policies opt for additional coverage for frozen pipes and water damage.

6. An insurance agent is a valuable resource to provide individuals with information on their protection of property. This includes specific things like insurance coverage and property damage.

7. Companies that provide insurance can offer various levels of protection and options to residents and renters of homes.

Will Damages Will Winter Insurance Cover?

Your home serves as a sanctuary to protect you from the elements, but it may not always emerge unharmed.

If your home experiences damages, such as a burst pipe or roof damage, you must contact your home insurance company quickly.

Understanding home insurance can be overwhelming, especially in the aftermath of a storm. It’s crucial to familiarize yourself with your home insurance policy ahead of time to avoid unnecessary stress during inconvenient situations.

From experience, the most essential time to know what your policy will cover is when you initially purchase the insurance. Winter insurance is vital for those living in areas where the weather can become harsh.

Check Your Declaration Page

If you have home insurance, you must be provided with a declaration page as part of your policy documentation.

Contained within it are the details of your policy’s coverage across the areas of dwelling, other structures, personal property, loss of use, liability, and medical coverage.

Although these categories are pretty straightforward, it may be beneficial to delve into further explanation. While the following explanations provide a general overview, it is advisable to independently verify the specifics of what your policy includes and excludes.

Again, this should be done at the time of purchase, not after dealing with problems in and around your home.

Dwelling Insurance

It is important to note that the coverage of your dwelling encompasses damage to your house.

For instance, if a strong wind rips shingles off your roof, this falls under your dwelling coverage.

Similarly, if a poorly insulated pipe freezes during a cold snap and floods your basement when it thaws, this is also included in your dwelling coverage.

If a wind-blown tree falls and lands on your screened porch, it would fall under your dwelling coverage.

Damage to your house is likely covered under your winter insurance dwelling coverage. Asking an insurance professional for assistance and verification is always advisable.Click To TweetOut Building

If you have other exterior buildings, such as a detached garage, fencing, a large shed, or a pool cabana, you would be covered under the section of your policy dealing with other structures.

Personal property

Personal property coverage is designed to protect your belongings in the event of damage caused by a claimable incident. For example, if a frozen pipe causes flooding in your basement and damages your home theater or couches, this type of coverage would apply to these items.

Liability

Property damage isn’t the only thing that comes up with insurance coverage.

Understanding liability coverages is crucial. Liability coverage protects you in the event someone gets hurt on your property. For example, someone sustains injuries from an accident on your front walk.

Due to the weather, a person slips and falls on the way to the front door or in your driveway. Maybe sleet has caused treacherous conditions. Liability insurance can protect you in such circumstances. There will be limits to the amount of protection you’re given, so it’s worth knowing.

It’s one of the questions in scenarios in an area with cold weather and winter storms.

Loss of use

If your home sustains significant damage, rendering it uninhabitable for some time, loss of use coverage can assist in offsetting the costs associated with securing alternative temporary accommodations.

For example, if you need to stay in a hotel down the road because your home is uninhabitable.

Several years ago, one of my clients selling their home was out of state. The oil tank was not filled when it should have been, causing the pipes to freeze. When I visited the house, I found it a flooded disaster.

Exclusions

Many homeowner’s policies have exclusions. Typically, they cover floods, mold, maintenance problems, or earthquakes. It’s essential to verify coverage for winter storm damages in your policy.

From experience, many homeowners do not realize that most home insurance policies do not cover the presence of mold. Over the years, I have been involved with numerous properties that experienced mold.

Selling a home with mold is always challenging as it causes tremendous uneasiness among potential home buyers. Buyers always require the mold to be remediated or get compensation for repairs.

Removing any house dangers is always a wise thing to do.

A key takeaway is to know that it’s unlikely your insurance policy will cover mold in the winter or otherwise.

The Enemy: Snow And Ice

The two things you must watch out for in winter are snow and ice. Snow can pile up on roofs and trees, collapsing roofs and broken limbs.

Once the snow melts, it can seep and even pour water into unprotected areas, like leaky roofs and septic systems.

Ice is another hazard, breaking tree limbs off (possibly on top of homes) and ripping gutters off eaves. It can also freeze pipes, causing them to burst and even creating walking hazards for you and your neighbors.

One of the more common things that can occur in the winter is ice dams. These little buggers can create quite a hassle for homeowners.

Most of the time, ice dams will be covered under your insurance policy, but it is worth checking. Read about what you should know about removing and preventing ice dams.

Look and bookmark this one – it will be well worth it! This will be one of the most comprehensive articles you will see from start to finish on preventing, removing, and then dealing with insurance claims on ice dams.

Fortunately, homeowners insurance covers a lot of these things. But it may not cover all of them, depending on your policy. You should also be aware that many insurers will be looking for negligence on your part.

They may not cover your claim if they find that you failed to take preventative measures.

What Winter Homeowners Insurance Covers

Your homeowner’s insurance policy will probably cover all direct damage from winter weather. This direct damage includes roof collapse from snow accumulation, tree limbs falling on your home, shingles being ripped off by winter storms, and burst pipes (in particular circumstances).

As discussed above, ice dams are one of the most common insurance items covered by winter weather damage.

Negligence – What Homeowners Insurance Does Not Cover

If winter weather, like a blizzard, comes roaring in and directly damages your house, you can expect the policy to cover it. But insurers rarely just cut you a check.

If winter weather, like a blizzard, comes roaring in and directly damages your house, you can expect the policy to cover it. But insurers rarely just cut you a check.

They will do their research to determine if the damage was caused directly by the weather.

They are searching for negligence – a situation where they can prove that you did not care for the standard care that the home and the grounds needed.

If it can show that the damage was avoidable through standard care, it may deny all or part of your claim.

They will look for negligence in some areas, including:

Your Trees

Trees need trimming occasionally as old limbs die and new limbs grow. Taking care of this trimming is part of owning a home.

If a limb falls on your house or your neighbors, the insurer will look for signs that you failed to keep the tree trimmed.

If you didn’t take care of the dead limbs, you could be liable for the damage.

Winter Storms

The insurer will look to see that you did everything reasonable to protect your home from an incoming storm.

If you left the garage door open for the snow to come pouring in, the insurer is unlikely to pay for the property that the snow damaged.

Your Home’s Pipes

Pipes susceptible to freezing need to be protected by the homeowner. Either the heat needs to be left on, the pipes need to be insulated, or the pipes need to be drained.

If they can prove that you failed to do any of these things when the risks of freezing were apparent, they can deny the claim. Using the garage door left open as an example, the insurance company could deny your claim if this caused your pipes to freeze and burst.

Ice

Your local government may have rules in place for ice and snow removal. You must take care of the ice and snow on your property in many places to protect those passing by, like on the sidewalks.

If you never shovel the snow and your neighbor falls, the insurer may not be willing to pay. Some states, including Massachusetts, have enacted laws that say you must keep your property and sidewalks safe.

If someone slips and falls on your property or the sidewalk, they can sue you and win. This law was changed a few years back by the Supreme Court. For many years, homeowners were not held liable.

Snow

Although the insurer may replace a roof that has caved in from excessive snowfall, this is only true if you take the necessary precautions to protect the roof. Did you remove as much snow as possible when you had the opportunity to?

Was the roof in good repair, or was it old and decaying? This is also true when the snow melts and seeps in. The insurer might not pay for the damage if the roof requires repair.

Miscellaneous

Do you know some other things many homeowners insurance policies do not cover? Here are some of the most common issues a homeowners insurance policy may not cover.

Always understand what your insurance policy covers and doesn’t cover!

What Happens When You File a Winter Insurance Claim?

When filing a claim for a covered loss, your insurance company typically reimburses you the replacement cost or the actual cash value.

If your insurance provider compensates you for the actual cash value, it will cover the worth of your possessions, deducting any depreciation, such as wear and tear. This amount will be less than what you would receive if you were compensated based on the replacement cost.

Replacement cost refers to the expense required to obtain a new, comparable item to replace what has been damaged or lost.

For instance, if a tree hits a deck during an ice storm or a pool table is damaged during a flood, the replacement cost is the money needed to purchase a new one of similar quality.

Similarly, when it comes to rebuilding a house, the replacement cost is the estimated amount necessary to reconstruct it to a similar quality standard.

Flood Insurance Is Separate

Remember that homeowner’s insurance does not protect you in a flood. When the weather warms up, and the snow melts, it can lead to overflowing drains and septic systems.

Remember that homeowner’s insurance does not protect you in a flood. When the weather warms up, and the snow melts, it can lead to overflowing drains and septic systems.

If you do not have flood insurance for your home, do not expect to be covered for the damage.

This is why insurers recommend a separate flood insurance policy for homeowners who live in areas where flooding – even from melting snow – is possible.

Flood insurance can be very costly. If you are in a flood plain and have a mortgage, your lender will probably require it.

What Should I Expect to Pay From The Damages

When making an insurance claim for damages that have occurred at your home and are covered by your insurance policy, the deductible is the only thing you should expect to pay.

Significant claim payments could also require that your mortgage company be placed on the check.

You should be prepared for this and ask your insurance provider beforehand. It is also possible that if both spouses own the home, both names will be placed on the check.

Speaking to your insurance company on how they release funds would also be prudent so you can be prepared to pay the contractors doing the work.

Ensuring that your insurance adjuster and contractor are on the same page regarding the cost to remedy damages is essential. The last thing you want to do is be short the necessary funds to pay for having all the work required to be completed.

Do Your Best And Make A Claim When Necessary

Ultimately, you can only do your best to keep your property in good condition. Regular maintenance is not complex; you can always pay someone else. This is something worth budgeting for.

If you wind up with winter damage, filing a claim as soon as possible is best. The adjuster will visit your home, examine the situation, and judge your claim.

Even if you have not kept your house up to snuff, you still may be able to get some money towards repairs. Most of the time, it is worth trying to get your damages covered as long as the cost of repairs is more than your deductible.

Keep in mind, however, that if you have had multiple claims filed for damages at your home, it is possible the insurance company could raise your rates. If you have minor damage to your home, it might make more sense to fix it yourself than to involve your insurance carrier.

How to Protect Your Home From Storm Damage

It is essential to have weather insurance to protect your house from damage. However, taking preventive measures to minimize the risk of damage from uncontrollable factors such as weather is even more crucial.

Homeowners can take steps to reduce the likelihood of their property being affected.

The Centers for Disease Control and Prevention offers excellent advice, including trimming overhanging branches on your property and dealing with roof problems immediately.

From my own experiences dealing with issues at my homes, keeping your gutters clean from debris is imperative. Clogged gutters can cause drainage problems, leading to water penetration.

Should an ice dam develop and obstruct your gutters, it can lead to water backing up onto your roof. If the water thaws and refreezes in that location, it can seep under the shingles and cause damage to your roof.

Ensuring that your attic has adequate insulation and proper ventilation is crucial. Most people don’t realize the lack of sound insulation in an attic is a leading cause of ice damming.

Additionally, insulating your pipes, particularly in colder areas of your home, can prevent damage from burst pipes.

While it’s impossible to guarantee that a winter storm won’t cause damage to your house, following these measures can help mitigate potential risks.

Additional Helpful Home Insurance Articles

- Homeowners insurance frequently asked questions via Progressive Insurance.

- A complete understanding of homeowners insurance via Wikipedia

Use these additional articles to understand how most insurance policies work and save yourself some money insuring your property.

About the Author: Bill Gassett, a nationally recognized leader in his field, provided information on whether winter insurance covers snow damage. He is an expert in mortgages, financing, moving, home improvement, and general real estate.

Learn more about Bill Gassett and the publications he has been featured in. Bill can be reached via email at billgassett@remaxexec.com or by phone at 508-625-0191. Bill has helped people move in and out of Metrowest towns for the last 38+ years.

Are you thinking of selling your home? I am passionate about real estate and love sharing my marketing expertise!

I service Real Estate Sales in the following Metrowest MA towns: Ashland, Bellingham, Douglas, Framingham, Franklin, Grafton, Holliston, Hopkinton, Hopedale, Medway, Mendon, Milford, Millbury, Millville, Natick, Northborough, Northbridge, Shrewsbury, Southborough, Sutton, Wayland, Westborough, Whitinsville, Worcester, Upton, and Uxbridge MA.